About OpenCongress

OpenCongress brings together official government data with news coverage, blog posts, public comments, and more to give you the real story behind what’s happening in Congress. Small groups of political insiders and lobbyists already know what’s really going on in Congress. Now, everyone can be an insider.

OpenCongress is a free, open-source, not-for-profit, and non-partisan web resource with a mission to make Congress more transparent and to encourage civic engagement. OpenCongress is a joint project of two 501c3 non-profit organizations, the Participatory Politics Foundation and the Sunlight Foundation. To read more about our mission, our open data sources, and how Congress works, see About OpenCongress. To read more about how individuals and organizations can use this site to find and share valuable info about their political interests, see How To Use OpenCongress.

Make Your Voice Heard

All too often, Congress is closed-off from meaningful public input. OpenCongress gives you free tools to contact Congress and open a dialogue with your elected officials. With your free “My OpenCongress” account, you can vote “aye” or “nay” on bills, give personal approval ratings to Members of Congress, post comments in discussion forums, and write your Members of Congress directly from OpenCongress

Watchdog Your Government

OpenCongress gives you the ability to oversee your elected officials and all of our Members of Congress. Together, we can build effective accountability and transparency in Congress. “My OpenCongress” profiles have “Watchdog” tools that allow you to compare your votes on bills with your Senators’ and Representative’s votes, as well as what other constituents in your state and Congressional district support and oppose — join or login to start Watchdogging and get local.

Track What’s Happening

Congress can be difficult to follow. OpenCongress provides easy ways to track all the things you care about. Subscribe to RSS feeds or email alerts to automatically receive updates on bills, votes, issues, and more. Also, you can join “My OpenCongress” to create a profile page that tracks all your political interests in one place — join or login, it’s free and takes less than a minute.

All the Best Info

OpenCongress and Formspal bring together all the best info about Congress and legal documents in one place. When you link to OpenCongress pages, your readers have access to not only the official details of bills and votes but also the big picture. Read more ways you can use OpenCongress.

Browse Non-Congressional Legal Templates and PDF Documents

At OpenCongress, we support free and accessible information to better inform and empower communities and individuals.

Check one of the links below to access fillable legal documents to suit your needs (or browse our full catalogs of legal templates and fillable PDF forms):

Bill of Sale Template – the document is used to record the ownership transfer of an item from one person (a seller) to another (a buyer). A bill of sale serves as legal evidence of many transaction types and protects both parties from any future misunderstandings. It should include all the essential details related to the transaction, including the seller’s and buyer’s contact information and a detailed description of the item to be sold.

Bill of Sale for Car – this form is designed to prove a change in the ownership of a car, motorcycle, or other motor vehicles. It ensures that the seller hands the certificate of title over to the buyer, and the buyer purchases the vehicle being fully aware of its condition (“as is”). In many states, it’s required to sign a bill of sale to register the vehicle in the Department of Motor Vehicles (DMV).

Last Will and Testament Form – a last will and testament is an essential legal instrument that arranges the property and assets division after a person passes away. This person, known as the testator, creates the last will to ensure that their real and personal property will be divided as they wish and not by the court order. Apart from naming the beneficiaries, the document is used to assign guardians for the testator’s minor children, if any.

Living Will Template – the document helps a person indicate end-of-life treatment they wish or do not wish to receive if they become terminally ill. A living will provides details relating to life-sustaining treatments and define the circumstances in which they should be used. A living will usually is a part of the Advance Health Care Directive along with a Medical Power of Attorney.

Power of Attorney Template – a power of attorney (POA) allows an individual (the principal) to appoint another person (the agent) to act as their representative. It comes in handy when a person cannot handle financial, business, or healthcare matters on their own. POAs allow the agent to assist the principal either on a short-term or a long-term basis. As a rule, a power of attorney loses its force when the principal becomes incapacitated.

Durable Power of Attorney Form – this form is used to make a power of attorney effective even after a person (the principal) becomes incapacitated. A durable power of attorney is an irreplaceable legal tool ensuring that a trusted person will manage the principal’s property and assets when the latter is no longer capable of doing that.

Small Estate Affidavit Form – if someone is sure about their inheritance rights and wants to avoid a lengthy probate process, they can use a small estate affidavit to claim the assets of a deceased person. However, as the name implies, this form can be used only for the small estate that is valued below a certain amount, varying from state to state.

Lease Agreement Template – this binding agreement helps build a strong legal basis for successful rental relationships between a landlord (also, a lessor) and a tenant (also, a lessee). A lease agreement should consist of all the essential terms and requirements, including rent amount, pet and smoking policy, late fees, and utilities, to avoid future misunderstandings.

Eviction Notice Template – if a landlord wants to evict a tenant, they should send an eviction notice first. An eviction notice, also known as a notice to quit, specifies why the tenant must vacate the rental premises. As a rule, it also provides ways to improve or cure the situation (except when a tenant commits a crime on the premises).

Release of Liability Form – the document ensures that one party, known as a releasor, will not sue another party, known as a release, who can be potentially liable. A release of liability can be used for both past and future events. This form is frequently used by business entities providing extreme activities to avoid responsibility for possible injuries or damage these activities can cause.

Promissory Note Template – a promissory note has a binding legal value and helps to ensure that the person giving the money will receive them back. A promissory note should contain all the crucial agreement’s terms, including the loan amount, repayment schedule, collateral (if any), interest rate, and late fees. If a promissory note includes collateral, it’s called a secured promissory note.

Non-Compete Agreement Template – this document is designed to prevent one party from competing with another party in the same industry or geographical area for a certain period of time. Companies usually use a non-compete agreement when hiring new employees. However, many states do not recognize non-compete clauses, so it’s essential to consult the state laws before preparing this agreement type.

Prenuptial Agreement Template – also known as a “prenup,” this agreement is signed by a couple who will get married. A prenup can be considered as a business partnership agreement between romantic partners, which manages financial responsibilities and obligations in the event of a divorce or death. Nevertheless, a prenuptial agreement cannot manage such issues as child custody and child support.

Operating Agreement Template – whether it’s a single-member or multiple-member limited liability company (LLC), their owners can use an operating agreement to clearly define all LLC members’ rights, obligations, and liabilities. This agreement is not required in every state, but it’s highly recommended for companies’ owners who want to set their own rules and procedures for the LLCs.

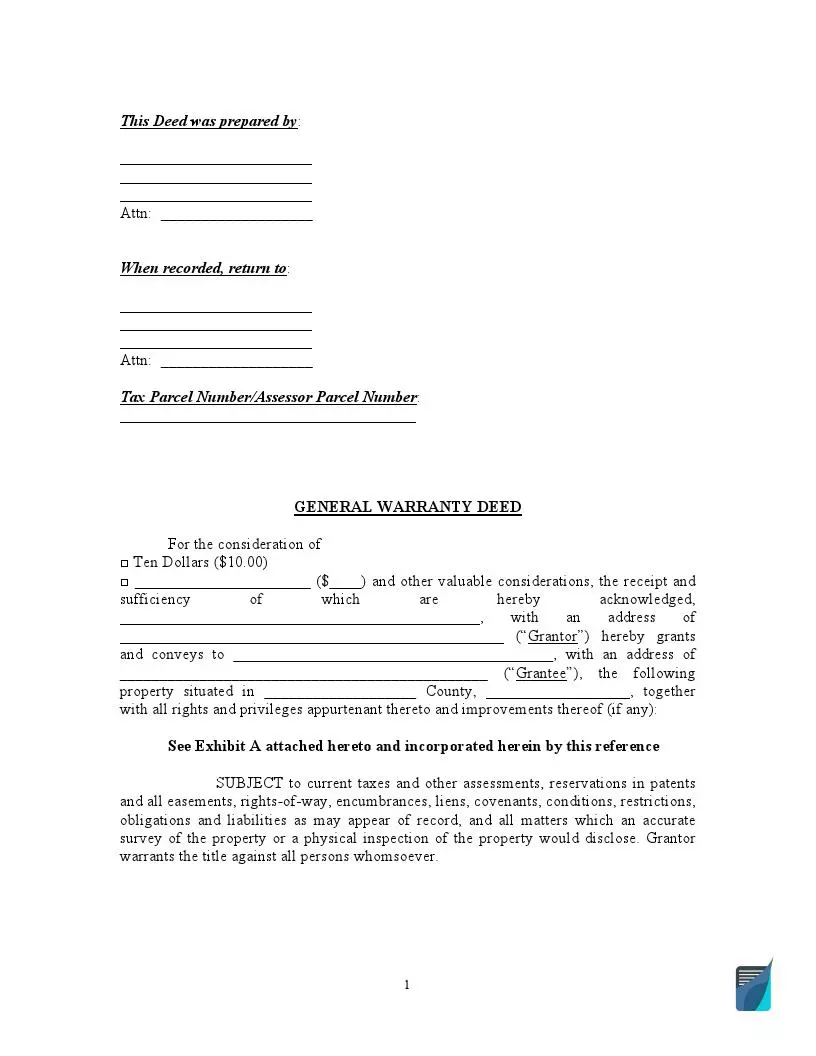

Quitclaim Deed Forms – also known as a “non-warranty deed,” a quitclaim deed is the least secure of all deed types. The form is used to transfer real estate ownership easily and quickly, but it doesn’t guarantee that the one who’s transferring has full rights to the property. That’s why a quitclaim deed is usually signed between individuals who can trust each other, for example, family members.

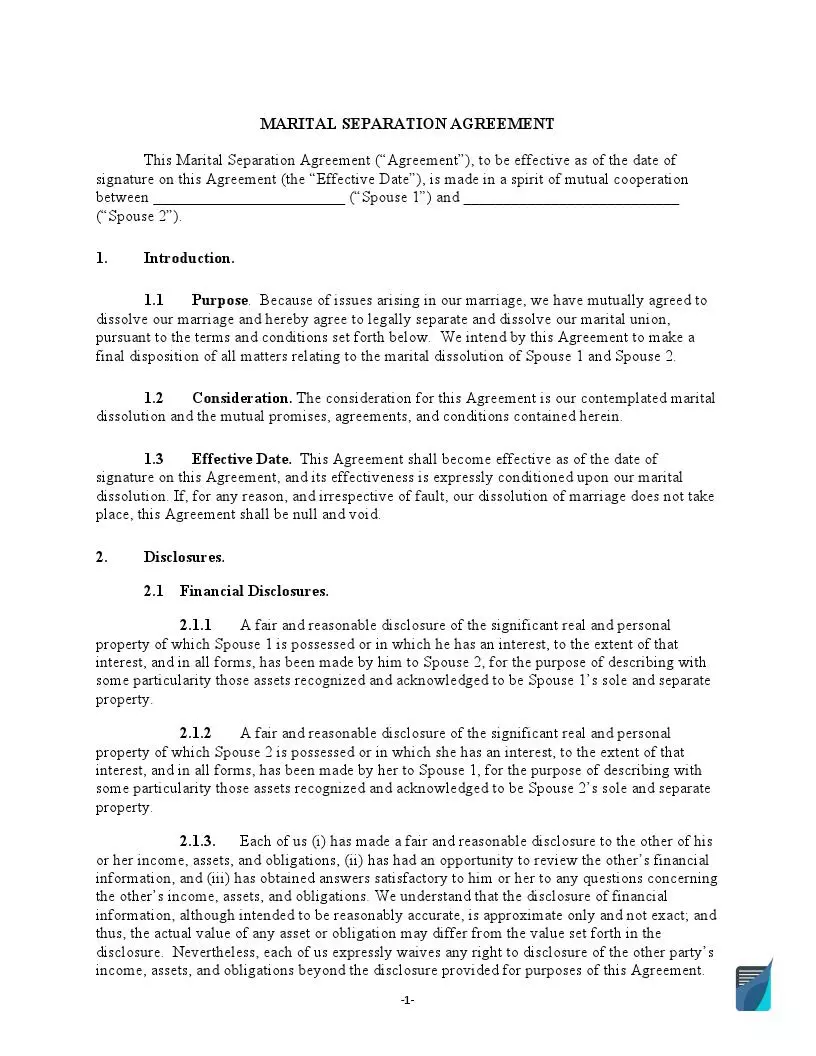

Marital Settlement Agreement Template – if a married couple decides to divorce, they don’t have to undergo an exhausting divorce process. With a marital (divorce) settlement agreement, they can agree in advance on such issues as assets and debts division, alimony, and child custody. Of course, it’s impossible to avoid court involvement entirely in this matter, but a marital settlement agreement can make a divorce a lot less stressful.

Non-disclosure Agreement Template – a non-disclosure agreement (NDA) allows the owner of confidential information to protect it from unauthorized usage. An NDA is frequently used when hiring new employees or establishing business partnership relationships. The agreement protects all sensitive data that can be shared between employees or business partners.

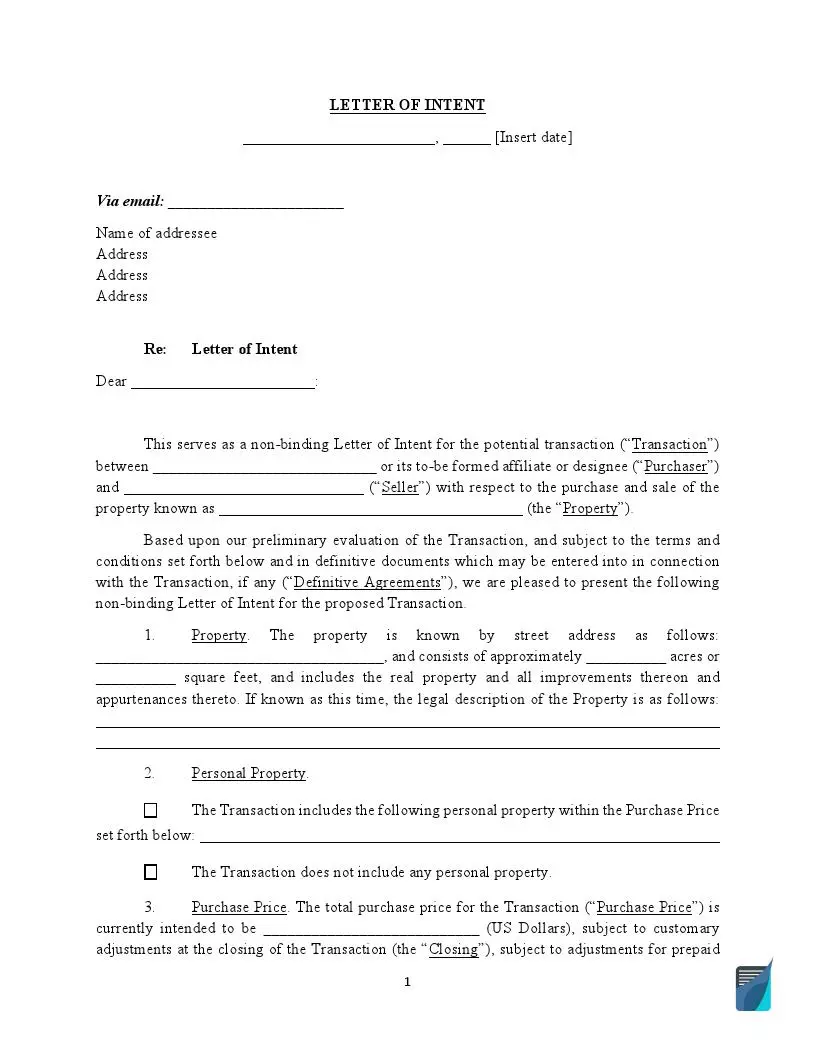

Letter of Intent Template – as the name implies, this document serves as a way to express an intention to do something. This intention can be related to various matters, from establishing cooperation between two parties to defining future purchase details. A letter of intent (LOI) is non-binding, but it’s helpful in terms of building a basis for the forthcoming definitive agreements.

Meeting Minutes Template – this document ensures that all the meeting decisions and outcomes are recorded and can be used in the future. Meeting minutes help not only inform the absent members about what happened during the meeting but also to track down the company’s or organization’s progress. Minutes should not include every detail of the meeting but rather outline key issues, votes, and plans.

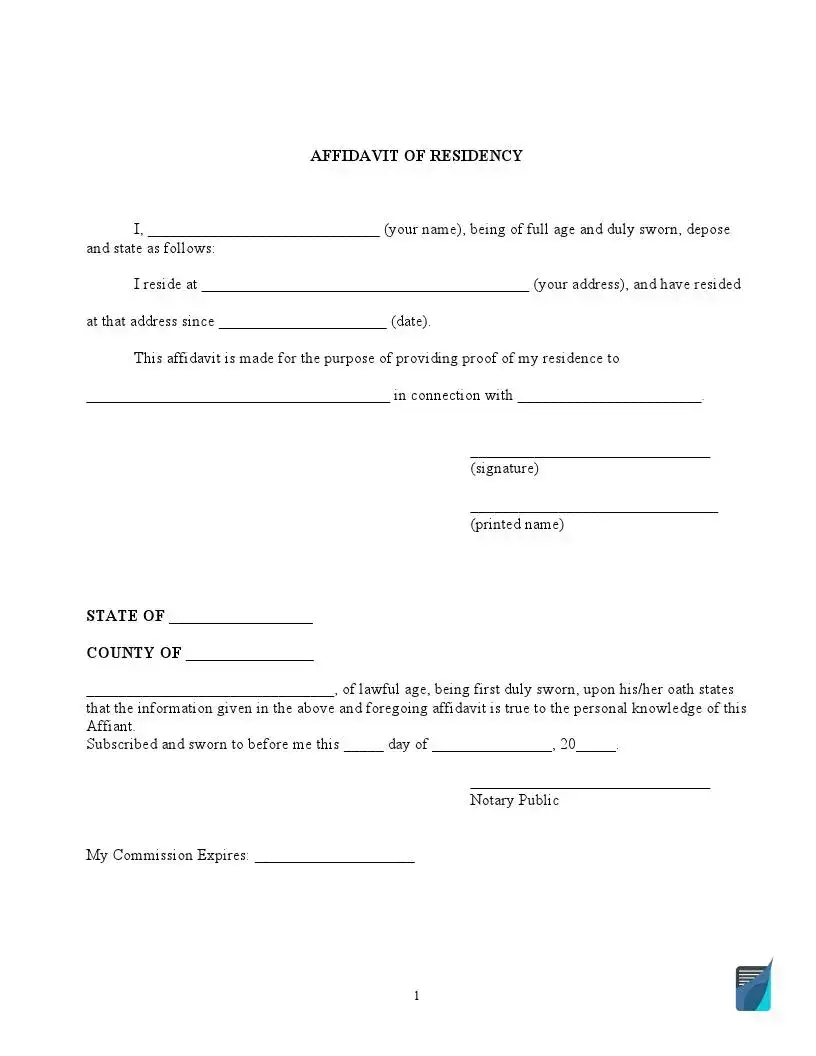

Affidavit Form – with an affidavit form, a person confirms under oath that the written statement is true. An affidavit can be used for many reasons such as verifying someone’s identity, attesting birth or death, or presenting formal statements as a witness. It’s a legally binding document and should be signed voluntarily and in the presence of a notary public.

Purchase Agreement Template – the agreement outlines the terms and conditions of a future transaction between a seller who wants to sell the property and a buyer who wants to receive the ownership rights. A purchase agreement should include the seller’s and buyer’s contact information, property description, purchase price, payment structure.

Loan Agreement Template – this document is an essential legal tool to outline the terms between lending and borrowing parties. The agreement proves that the money is borrowed and not gifted and ensures the borrower will pay them back. A loan agreement will come in handy if a person plans to set up a business, buy expensive equipment, pay for the treatment, or cover the tuition.

Bill of Sale Forms

On average, there are 1.88 vehicles per American household, which means that there are almost two buy-sell transactions between parties during the lifetime and US regulations require people to have a proper bill of sale.

We have put together a list of the most popular bill of sale templates (that are fillable, editable, and downloadable) to help you better handle the sales process and ownership transfer of your property.

The Most Widely Used Bill of Sale Forms

A bill of sale serves as essential evidence and protection of the transaction between a seller and buyer. In many states, it’s required to sign a bill of sale, for example, to register a purchased car in the Department of Motor Vehicles (DMV). However, a bill of sale can be helpful not only to sell a used car but also to buy or purchase other types of vehicles (check our vehicle bill of sale page), items, and even boats. The forms below are the most widely used in the U.S. when it comes to recording a transaction.

One of the most popular bill of sale forms is a Bill of Sale for Boat. According to the National Marine Manufacturers Association (NMMA), sales of new powerboats in the U.S. increased in 2020 by around 12% compared to 2019. Outdoor activities are becoming more and more widespread due to the pandemic, so it’s quite an understandable trend. Thus, a boat bill of sale can come in handy when someone wants to discover the benefits of the open air by buying a personal watercraft.

Another widely used bill of sale form is a Bill of Sale for Trailer. A trailer is any structure that can be pulled by a vehicle, for example, travel trailers or mobile homes, so it’s very convenient to have one in the garage. A trailer bill of sale is similar to motor vehicle and boat bills of sale, as it includes the same details such as vehicle identification number (VIN), make, model, and year of manufacturing.

Some states, for example, Texas, require you to sign a bill of sale to buy or sell cars and boats. To prove that a transaction has taken place, a Texas Bill of Sale must include the item’s description, condition, VIN or HIN (if it’s a car or boat), transaction date, purchase price, and the parties’ contact information. Depending on a transaction type, a Texas bill of sale should be prepared along with the vessel, vehicle, or firearm registration forms.

In Florida, you need to prepare and sign a Florida Bill of Sale to legally record the item’s sale or purchase. The document should include the parties’ names and addresses, item description, transaction date, and purchase amount. It’s necessary to prepare the specific bill of sale forms when buying or selling a motor vehicle, boat, or firearm. These forms should be supported by Florida vehicle or boat registration documents.

If it’s necessary to prove a legal sale or purchase in Missouri, a Missouri Bill of Sale will ensure that the deal is finalized and secured. This document serves as a receipt of a transaction and should provide all details regarding a seller, buyer, item, purchase date, and price. In some cases, it’s necessary to notarize a bill of sale in Missouri, for example, when selling or buying a motor vehicle.

State Bill of Sale Templates by Type

A bill of sale is not only a way to get receipts confirming transactions but also crucial evidence to avoid future misunderstandings. Each transaction type usually needs a specific bill of sale form. Some of them may have to be notarized and signed by both parties, and others may be legally required to prove the ownership change or register the vehicle. Sometimes, you know what bill of sale type you need but cannot find the form appropriate in the state you live in. Below you will find a list of all essential state bill of sale forms divided by types.

- Alabama Boat Bill of Sale

- Alabama Firearm Bill of Sale

- Alabama Vehicle Bill of Sale

- Firearm Bill of Sale AZ

- AZ DMV Bill of Sale

- Boat Bill of Sale Arkansas

- Vehicle Bill of Sale Arkansas

- Trailer Bill of Sale AR

- California Vehicle Bill of Sale

- California Motorcycle Bill of Sale

- Car Bill of Sale Colorado

- Motorcycle Bill of Sale Colorado

- Colorado Trailer Bill of Sale

- DMV Bill of Sale CT

- Florida Boat Bill of Sale

- Florida Firearm Bill of Sale

- Motorcycle Bill of Sale Florida

- Car Bill of Sale Florida

- Florida Bill of Sale for Trailer

- GA Boat Bill of Sale

- Georgia Firearm Bill of Sale

- Georgia Auto Bill of Sale

- Motorcycle Bill of Sale GA

- Georgia Trailer Bill of Sale

- Idaho DMV Bill of Sale

- Firearm Bill of Sale IL

- Illinois Vehicle of Sale

- Indiana Gun Bill of Sale

- Indiana BMV Bill of Sale

- Iowa Car Bill of Sale

- Kansas Bill of Sale Boat

- Kansas Bill of Sale for Car

- Boat Bill of Sale Louisiana

- Firearm Bill of Sale Louisiana

- Louisiana Auto Bill of Sale

- Car Bill of Sale Maine

- Maryland Boat Bill of Sale

- Maryland MVA Bill of Sale

- Massachusetts Boat Bill of Sale

- Massachusetts Car Bill of Sale

- Boat Bill of Sale MI

- Car Bill of Sale Michigan

- MN Boat Bill of Sale

- Boat Bill of Sale Mississippi

- MO Boat Bill of Sale

- Firearm Bill of Sale Missouri

- Missouri Auto Bill of Sale

- Montana DMV Bill of Sale

- Car Bill of Sale Nebraska

- Nevada Firearm Bill of Sale

- NV DMV Bill of Sale

- Car Bill of Sale NJ

- Trailer Bill of Sale NJ

- New Mexico Vehicle Bill of Sale

- DMV Bill of Sale NY

- Trailer Bill of Sale NY

- Boat Bill of Sale NC

- Gun Bill of Sale NC

- NC Vehicle Bill of Sale

- NC Bill of Sale for Trailer

- Ohio Gun Bill of Sale

- Car Bill of Sale Ohio

- Auto Bill of Sale Oklahoma

- Oregon Boat Bill of Sale

- Oregon DMV Bill of Sale

- Bill of Sale for Car PA

- SC DNR Boat Bill of Sale

- Firearm Bill of Sale SC

- SC DMV Bill of Sale

- South Dakota Vehicle Bill of Sale

- TN Boat Bill of Sale

- Gun Bill of Sale TN

- Auto Bill of Sale TN

- TN Trailer Bill of Sale

- Boat Bill of Sale Texas

- Texas Firearm Bill of Sale

- Vehicle Bill of Sale Texas

- Texas Bill of Sale for Trailer

- Utah Gun Bill of Sale

- Utah DMV Bill of Sale

- VT DMV Bill of Sale

- Firearm Bill of Sale VA

- Vehicle Bill of Sale Virginia

- Washington Vehicle Bill of Sale

- West Virginia DMV Bill Of Sale

- Boat Bill of Sale Wisconsin

- Vehicle Bill of Sale Wisconsin

Bill of Sale Forms by State

Bill of sale forms can be used for different purposes, from selling personal property, like furniture, to transferring the ownership of a used car, trailer, or boat. Depending on the state, their contents may vary a little. Still, as a general rule, they include similar information about a seller and buyer, the item to be sold, its condition, as well as sales tax details. A bill of sale should specify whether the item is subject to sales tax, its amount, and who will be responsible for payment. Look through the list below to find and create your local bill of sale form.

- Alabama Bill of Sale

- Alaska Bill of Sale

- Arizona Bill of Sale

- Bill of Sale Arkansas

- CA Bill of Sale

- Bill of Sale Colorado

- Bill of Sale CT

- Delaware Bill of Sale Form

- GA Bill of Sale

- Hawaii Bill of Sale

- Bill of Sale Idaho

- Illinois Bill of Sale

- Bill of Sale Indiana

- Iowa Bill of Sale

- Bill of Sale Kansas

- Bill of Sale KY

- Louisiana Bill of Sale

- Maine Bill of Sale

- MD Bill of Sale

- MA Bill of Sale

- Michigan Bill of Sale

- Bill of Sale MN

- Mississippi Bill of Sale

- Montana Bill of Sale

- Nebraska Bill of Sale

- Bill of Sale NV

- NH Bill of Sale

- NJ Bill of Sale

- Bill of Sale NM

- Bill of Sale NY

- NC Bill of Sale

- ND Bill of Sale

- Ohio Bill of Sale

- Oklahoma Bill of Sale

- Oregon Bill of Sale

- PA Bill of Sale

- Rhode Island Bill of Sale

- SC Bill of Sale

- SD Bill of Sale

- Bill of Sale TN

- Utah Bill of Sale

- VT Bill of Sale

- Virginia Bill of Sale

- Bill of Sale WA

- Bill of Sale WV

- Wisconsin Bill of Sale

- Wyoming Bill of Sale

Bill of Sale Types

Bills of sale are divided into types depending on the property you want to sell or buy. Each document should always include a detailed description of this property. Selling a car or boat requires knowing such things as a vehicle identification number (VIN) or hull identification number (HIN). If you want to sell an animal, like a horse or dog, you should include their breed, gender, and weight. These details are essential for an accurate record of the transaction. If you are looking for a specific bill of sale type, you can check the list below and choose the appropriate one.

- FAA Aircraft Bill of Sale

- Bill of Sale for Artwork

- Bill of Sale ATV

- Bike Bill of Sale

- Bill of Sale for Business

- Bill of Sale for Cat

- Dirtbike Bill of Sale

- Bill of Sale for Dog

- Bill of Sale for Equipment

- Gun Bill of Sale

- Furniture Bill of Sale

- Bill of Sale Generic

- Bill of Sale Golf Cart

- Equine Bill of Sale

- Bill of Sale for Jet Ski

- Cattle Bill of Sale

- Bill of Sale for Mobile Home

- Scooter Bill of Sale

- Bill of Sale Motorcycle

- Bill of Sale RV

- Snowmobile Bill of Sale Template

- Bill of Sale for Tractor

Sample:

If you’d like to get a better idea of what kind of bill of sale forms we have on our website, check out this sample below:

.

.

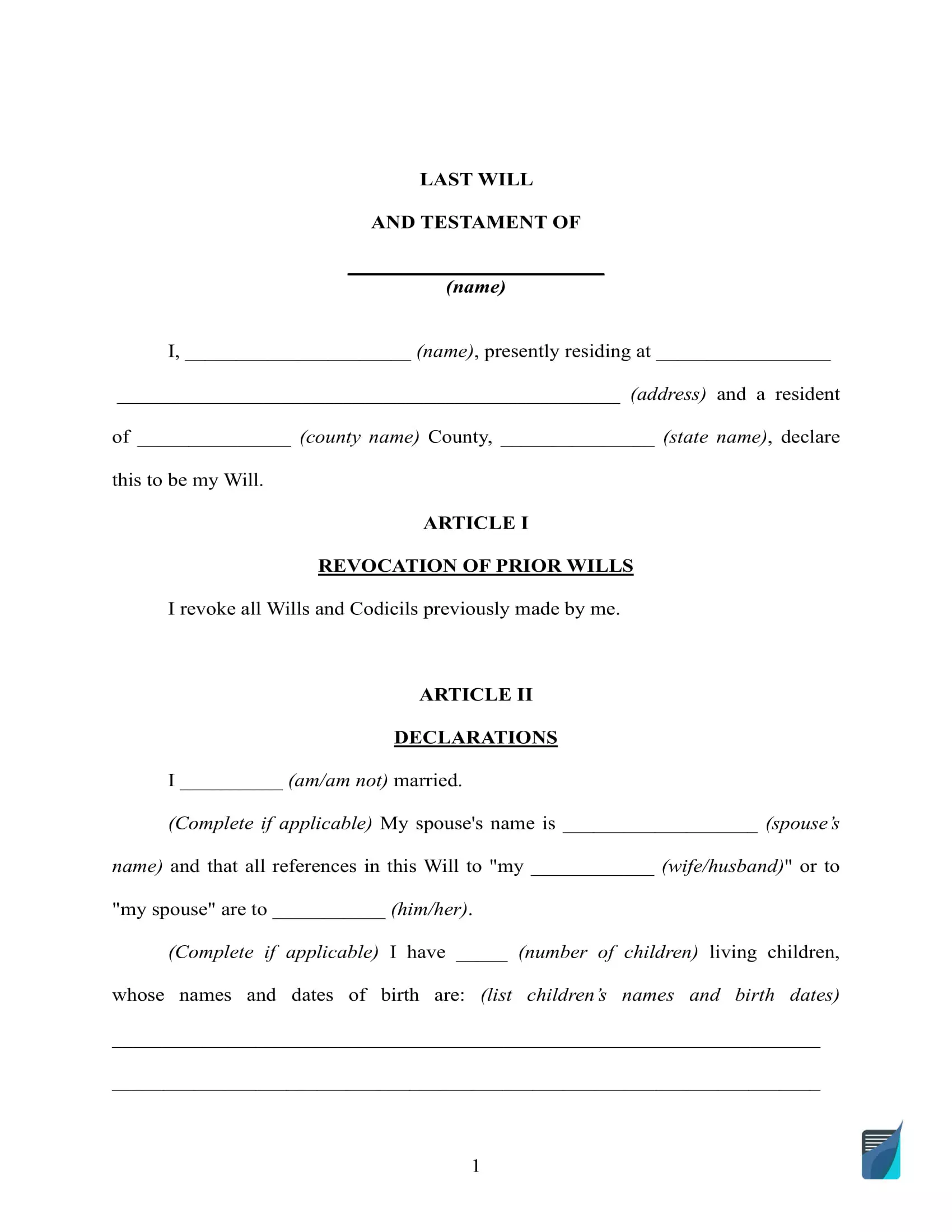

Last Will and Testament

Another thing that we have decided to provide to our communities is the variety of estate planning documents, especially focusing on high-quality customizable last will and testament templates. Click any of the links below to learn more about last wills and testaments in your state and download a proper template.

Popular State Last Will Forms

A last will and testament arranges the property and assets division among beneficiaries after a person’s death. If you want to decide who will get your personal and real property, you’re recommended to create one. A last will form has a generally accepted structure. It includes the testator’s (the one who is leaving the will) contact details, their marital status, and children, as well as beneficiaries’ names and executor’s contact information. However, signing requirements may differ from state to state. That’s why it’s essential to consult your state laws and family attorney to prepare a valid legal document. The following states have more requirements to consider when writing a last will, so these forms are considered to be more in demand.

To create a Florida Will Form, you need to choose the right personal representative. The state of Florida requires them to be either a Florida resident or the testator’s close relative, including spouse, parent, or child. It’s crucial to remember that the testator may have to change the representative if they decide to move to another state. A Florida last will and testament must be in writing and signed in the presence of two witnesses who also have to sign the will.

If you live in Texas, you are allowed to prepare a Last Will and Testament Texas even you are under the age of 18 but serving in the armed forces or lawfully married. Texas law also recognizes holographic, or handwritten, wills but they must be created entirely in the testator’s handwriting. Otherwise, the testator will have to sign the document in the presence of witnesses.

You can use a North Carolina Will Form if you are a North Carolina resident. You need to comply with all standard requirements like legal age and sound mind and list the beneficiaries and your relationship to them. In North Carolina, a beneficiary may also be a witness along with two other witnesses. It’s also possible to prepare a handwritten last will in North Carolina, as well as a nuncupative (oral) will.

Preparing a New York Will includes basic requirements related to the testator’s age and capability. However, state signing requirements are a bit different. A New York last will may be signed either by the testator or by another person in the presence of the testator. Handwritten and oral wills are valid in New York state only under limited circumstances, for example, if a testator is a member of the armed forces and prepares the last will during war or armed conflict.

Last Will Forms by State

Other states have more or less similar requirements: a testator must be at least of age 18, of sound mind, understanding what a last will is and why he or she is creating it, sign the document in the presence of witnesses, and notarize it (if required). No matter in which state you create the document, it must include the following information: your assets and debts, beneficiaries’ names, executor’s details, and guardian for minor children, if any. If you comply with your state requirements, you will get a legal document that is likely to be valid in other states should you decide to relocate.

- Alabama Will

- Last Will and Testament Alaska

- Arizona Last Will and Testament

- Arkansas Will

- Colorado Will Template

- Connecticut Will Form

- Delaware Will

- Georgia Will

- Last Will and Testament HI

- Idaho Will Form

- Illinois Will

- Indiana Will Form

- Iowa Will Form

- Kansas Will

- Kentucky Will Form

- Last Will and Testament Louisiana

- Maine Wills

- Last Will and Testament Maryland

- Last Will and Testament Massachusetts

- Michigan Will Template

- MN Will Form

- Wills in Mississippi

- Missouri Will Form

- Wills in Montana

- Nebraska Will

- Nevada Will Form

- Wills in NH

- NJ Will

- New Mexico Will

- ND Last Will and Testament Form

- Ohio Will

- Will Oklahoma

- Oregon Will Form

- Pennsylvania Will Template

- RI Wills

- Last Will and Testament SC

- Last Will SC

- Last Will and Testament Tennessee

- Last Will and Testament Utah

- Last Will Vermont

- Virginia Will

- Washington State Will

- WV Wills

- Last Will and Testament Wisconsin

- Wyoming Will Form

Last Will Attachments

If you decide to change something in your last will, you will need to use an addendum to a will. A codicil is a supplement allowing a testator to make amendments to their last will or revoke it. It should be executed with the same formalities as a last will and include the testator’s contacts, original will’s details, and a list of amendments. If you want to speed up the probate process and prove the will’s authenticity, you may use a self-proving affidavit. It should be signed by two witnesses confirming that a last will is prepared voluntarily and in sound mind.

Sample Will Template

Here’s a sample last will template to give you a better understanding of how the final document is going to look like:

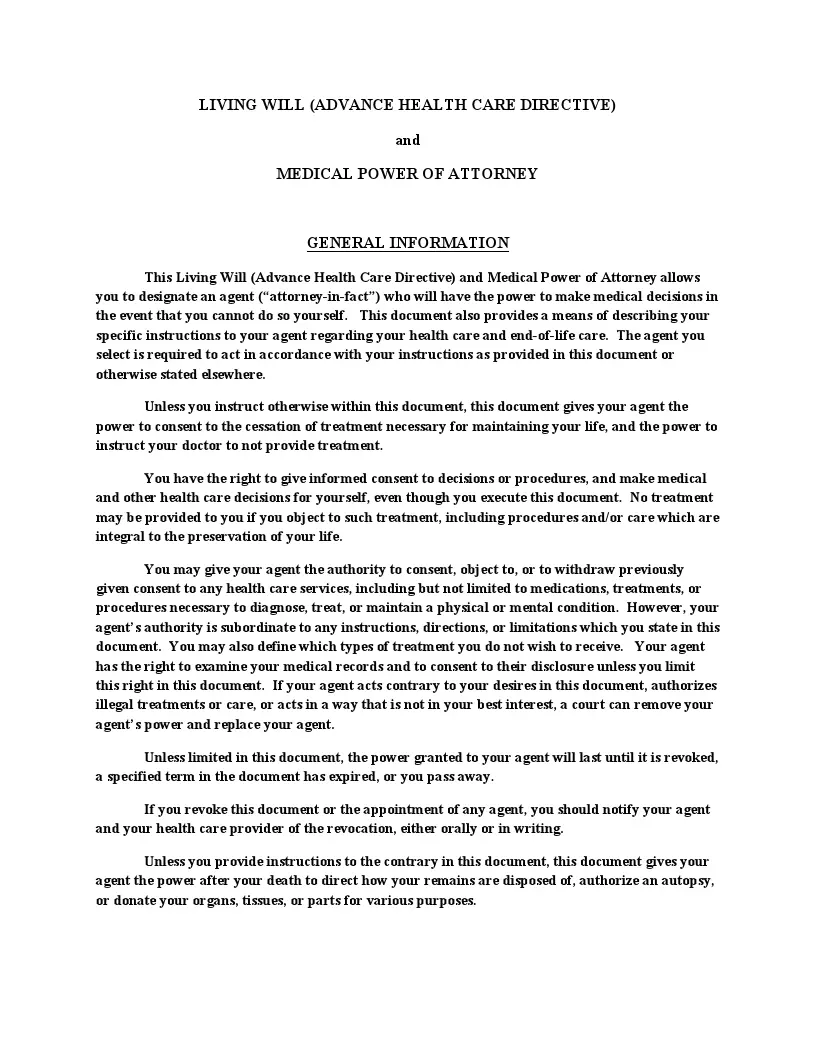

Living Will

If you’re looking for a valid living will template, we’ve got you covered too. A living will form is a special legal document that outlines an individual’s wishes regarding medical treatments that may prolong or save their life. Our living wills are created to fit the legal requirements in your state.

Popular State Living Will Forms

Unlike a last will, a living will addresses not your assets or property but your health. The document determines an individual’s (principal’s) preferences related to health care decisions if he or she becomes terminally ill or incapacitated. Your family and physicians will know for sure what end-of-life care you would like to receive with a living will form. The document provides essential details regarding life-sustaining treatments and circumstances they should or should not be used. So, you have to be very careful when creating one. The following state forms are widely used in the U.S. Check their requirements and terms if you live in one of these states.

If you live in Florida, you are recommended to use a Living Will Form Florida. It’s usually supported by a medical power of attorney, allowing you to appoint a health care surrogate to act as your representative. Together, these documents constitute an advanced health care directive. A Florida living will is a binding legal document and requires to be signed in the presence of two witnesses. A Florida living may lose its force if the principal becomes pregnant.

Apart from basic elements, an Ohio Living Will may include additional information about anatomical gifts and organ donation. If you want to become an organ donor, you should also complete a State of Ohio Living Will Declaration Notice. An Ohio living will may also be supported by a medical power of attorney. In any case, the documents have to be signed in the presence of two witnesses or a notary public.

To properly communicate your wishes regarding end-of-life care in Texas, you need to prepare a Living Will Form Texas, also known as Directive to Physicians and Family or Surrogates. This directive defines life-prolonging treatments and medical decisions if the principal cannot take care of themselves due to incapacity or terminal illness. A Texas living will must be signed in the presence of two witnesses, and a notary public presence is optional.

In Maryland, if you want to provide your family and physician with instructions for end-of-life care, you will need a Living Will Form Maryland, also called a Maryland Advanced Health Care Directive. You are free to customize this document as long as it perfectly fits your needs. You can include a health care agent or strike out this section if you do not need to appoint one. When the document is ready, you will have to sign it in the presence of two witnesses.

A Living Will New York allows a New York resident to specify every medical decision their physician can make if that person is incapacitated or has a severe illness. The document outlines life-sustaining and pain-relief instructions, but it’s also possible to include anatomical donation provisions. If you live in New York, you may choose to prepare an advanced directive and appoint your health care representative as well.

Living Will Forms by State

Depending on the state, a living will be called an advanced health care directive. Some states treat them as the same documents providing the individual’s wishes related to end-of-life care and life-sustaining treatments. However, in many states, an advanced health care directive is a more comprehensive document and includes a medical power of attorney. A medical POA allows you to appoint a trusted person to handle health care decisions on your behalf. You need to consult the state laws to decide which legal document is better to prepare. Below you will find the list of specific state living will forms.

- Alabama Living Will

- Arizona Living Will

- California Living Will Form

- Living Will Form Colorado

- Georgia Living Will Form

- Illinois Living Will

- Indiana Living Will

- Kentucky Living Will

- Living Will ME

- Living Will Form Michigan

- Missouri Living Will Form

- Living Will Form NJ

- NC Living Will

- Oklahoma Living Will

- Pennsylvania Living Will Form

- SC Living Will

- TN Living Will

- Living Will Virginia

- Living Will Form Washington State

Sample Living Will

Power of Attorney

A power of attorney is a legal document that describes the relationships between two parties, the principal and the agent, or, as it is commonly referred to, the attorney-in-fact. When signed, this document transfers the ability to represent the principal in decision-making to the attorney-in-fact. Get the latest PoA forms by using one of the provided links below

The Most Widely Used Power of Attorney Forms

A power of attorney is a written authorization for one person, known as the agent or proxy, to act on behalf of another person, known as the principal. This document gives the agent authority to represent the principal in various circumstances. Depending on its type, a power of attorney may provide limited powers or grant the general authority. In any case, you need to appoint a trusted person who will not benefit from the provisions. Below you will find the most widely used power of attorney forms.

In order to grant your agent the authority to make medical decisions, you are expected to use a Medical Power of Attorney Template. This document is also considered durable and aims at securing your health matters in the unfortunate event of severe illness or incapacity. You can provide your agent with an extended authority to act on your behalf, including withdrawing artificial life-sustaining treatments, or you may list only several powers.

If you are a California resident looking for a medical POA, you are recommended to take advantage of a California Medical Power of Attorney. A California medical power of attorney has specific requirements regarding the agent appointment. In California, you cannot appoint your supervising health care provider or any employee of the medical institution where you are receiving treatments as your health care proxy.

In case you need a general POA in California, you can use a Power of Attorney California. A California power of attorney must be created by a person of legal age and sound mind. The document can give your agent a wide variety of powers to execute, but you are free to list only several of them. Apart from the principal, a California POA must be signed by two witnesses or a notary.

If you live in the state of Texas, you should create a Texas Power of Attorney. It will help you arrange your financial activities, for example, signing documents or paying bills, when you are absent or cannot do it yourself for other reasons. If you are not sure what powers to include in a Texas POA, you should consult an attorney who will help you understand the powers you are giving to the agent.

Sometimes, you need to appoint a person to act on your behalf only in a specific case or for a limited period of time. That’s when you need to create a Limited Power of Attorney. This form allows you to list your agent’s functions and not grant them full authority. You can also specify a period of time your power of attorney will be effective.

State Power of Attorney Forms by Type

Powers of attorney serve as solid legal instruments managing financial activities or health care decisions when a person cannot handle them on their own. A POA becomes invalid if the principal is incapacitated (if it’s not a durable POA) or dies. At the same time, a POA can have an ending date or be revoked anytime. It can be challenging to find a suitable state POA form, not to mention appropriate types. That’s why we’ve gathered essential state POAs by types, a list of which you will find below.

- AZ Durable Power of Attorney

- Medical Power of Attorney AZ

- California Durable Power of Attorney

- Colorado Durable Power of Attorney

- Colorado Medical Power of Attorney

- Florida Durable Power of Attorney

- Medical Power of Attorney Florida

- Durable Power of Attorney Georgia

- Medical Power of Attorney Georgia

- Medical Power of Attorney Idaho

- Illinois Durable Power of Attorney

- Illinois Power of Attorney for Health Care

- Indiana Durable Power of Attorney

- Indiana Health Care Power of Attorney

- Kansas Durable Power of Attorney

- Maine Health Care Advance Directive Form

- Durable Power of Attorney Maryland

- Medical Power of Attorney Maryland

- Massachusetts Durable Power of Attorney Form

- Massachusetts Health Care Proxy Form

- Michigan Durable Power of Attorney

- Michigan Medical Power of Attorney

- Medical Power of Attorney MN

- Missouri Durable Power of Attorney

- Missouri Medical Power of Attorney

- Durable Power of Attorney NJ

- Health Care Proxy NJ

- New York Durable Power of Attorney

- New York Health Care Proxy Form

- NC Durable Power of Attorney

- Medical Power of Attorney NC

- Durable Power of Attorney Form Ohio

- Ohio Medical Power of Attorney

- Oklahoma Durable Power of Attorney

- Oregon Durable Power of Attorney

- Health Care Power of Attorney Oregon

- Pennsylvania Durable Power of Attorney

- Health Care Proxy PA

- Durable Power of Attorney SC

- Health Care Power of Attorney SC

- Tennessee Durable Power of Attorney

- TX Durable Power of Attorney

- Texas Medical Power of Attorney

- Medical Power of Attorney Utah

- Virginia Durable Power of Attorney

- Virginia Health Care Power of Attorney

- Durable Power of Attorney Form Washington State

- Power of Attorney for Health Care WI

Power of Attorney Forms by State

The structure of powers of attorney is more or less the same. You need to include information about yourself, your agent, alternate agent (if any), governing law, and execution date. But you have to remember that signing requirements can vary from state to state. Usually, you need two witnesses or a notary public. That’s why it’s crucial to check the local laws and choose a POA form specific to your state. You can check the forms below if you need a state POA form.

- Alabama Power of Attorney

- Alaska Power of Attorney

- Arizona Power of Attorney

- Arkansas Power of Attorney

- Power of Attorney Form Colorado

- Power of Attorney Form CT

- Power of Attorney Delaware

- Power of Attorney Florida

- Power of Attorney GA

- Hawaii Power of Attorney

- Idaho Power of Attorney

- Illinois Power of Attorney

- Power of Attorney Form Indiana

- Iowa Power of Attorney Form

- Kansas Power of Attorney

- Power of Attorney Kentucky

- Louisiana Power of Attorney

- Maine Power of Attorney

- Power of Attorney Forms Maryland

- Massachusetts Power of Attorney

- Power of Attorney Form Michigan

- MN Power of Attorney Forms

- Power of Attorney Mississippi

- Power of Attorney Form Missouri

- Power of Attorney Form Montana

- Power of Attorney Form Nebraska

- Power of Attorney Form Nevada

- New Hampshire Power of Attorney

- NJ Power of Attorney Forms

- NM Power of Attorney

- Power of Attorney Form New York

- North Carolina Power of Attorney

- Power of Attorney Form ND

- Ohio Power of Attorney Form

- Power of Attorney Form Oklahoma

- Oregon Power of Attorney

- Pennsylvania Power of Attorney Forms

- Rhode Island Power of Attorney

- SC Power of Attorney

- South Dakota Power of Attorney

- Power of Attorney Form for Tennessee

- Utah Power of Attorney Form

- Vermont Power of Attorney

- Power of Attorney Virginia

- Washington State Power of Attorney

- Power of Attorney Form WV

- Wisconsin Power of Attorney

- Wyoming Power of Attorney

Power of Attorney Types

Depending on the circumstances, you may need to prepare different powers of attorney. The main four POA types include general power of attorney, limited power of attorney, durable power of attorney, and springing power of attorney. We’ve mentioned durable and limited POAs above. Unlike a durable POA, a springing POA is a document that comes into force only if the principal becomes incapacitated. That’s why medical POAs are often made springing. A general POA, in its turn, is a comprehensive document containing an extensive list of powers granted to the agent. No matter what POA type you need, you should always choose a reliable person as your agent.

- Power of Attorney Template for Children

- General Power of Attorney

- Power of Attorney IRS

- Vehicle Power of Attorney

- Power of Attorney for Real Estate

- Revocation of Power of Attorney

- Power of Attorney for Tax

Sample PoA:

Small Estate Affidavit

Another document you might want to have ready when working on estate planning and estate distribution is a small estate affidavit. Browse the small estate affidavit forms that we have prepared for you below.

Popular State Small Estate Affidavit Forms

A small estate affidavit allows a legal heir to claim the inheritance rights. This affidavit helps expedite a probate process but can only be used for an estate that is lower than a certain amount. This amount depends on the state and ranges from $5000 to $100000. Sometimes, you need to attach a death certificate of the person who left the inheritance (the decedent). To prepare a small estate affidavit properly, you need to consult your local requirements. The following small estate affidavit forms are more in demand than others. Check their requirements if you a resident of one of these states.

If you live in California, you may face some additional considerations when preparing a California Small Estate Affidavit. In California, you are required to attach a death certificate to your small estate affidavit form. The document should be filed only 40 days after a person’s death and signed in the presence of an attorney. The maximum amount of the estate can reach up to around $170000. There are also some additional forms you will have to fill out.

In Illinois, you may use an Illinois Small Estate Affidavit to claim the inheritance rights to personal property. The maximum value of the property should not exceed $100000. An Illinois small estate affidavit cannot include the real property. To fill out this form, you will also need to list the decedent’s debts and unpaid bills.

If a person dies without a will in Texas, their heirs can prepare a Texas Small Estate Affidavit. To file a small affidavit in Texas, it’s necessary to wait 30 days from the date of the person’s death. The maximum amount of the estate should not exceed $75000. A Texas small estate affidavit should be approved by the probate court in the county where the person dies.

Small Estate Affidavit Forms by State

Every small estate affidavit form includes the contacts of a legal heir, their relationship to the decedent, the decedent’s details, description of their property and assets, how it should be divided among heirs, debts, and funeral expenses. However, your state laws can influence the preparation process in terms of waiting periods, signing requirements, and additional documents to be attached. We’ve prepared a list of all necessary state small affidavit forms below as a matter of convenience.

- Alabama Small Estate Affidavit Form

- Arizona Small Estate Affidavit

- Arkansas Small Estate Affidavit

- Colorado Small Estate Affidavit

- Florida Small Estate Affidavit Form

- Small Estate Affidavit Georgia

- Small Estate Affidavit Idaho

- Small Estate Affidavit Form

- Iowa Small Estate Affidavit

- Small Estate Affidavit Kansas

- Small Estate Affidavit Louisiana

- Maryland Small Estate Affidavit

- Massachusetts Small Estate Affidavit

- Michigan Small Estate Affidavit

- Minnesota Small Estate Affidavit

- Small Estate Affidavit Mississippi

- Small Estate Affidavit MO

- Nebraska Small Estate Affidavit

- Small Estate Affidavit Nevada

- NJ Small Estate Affidavit

- Small Estate Affidavit New Mexico

- Small Estates Affidavit NY

- North Carolina Small Estate Affidavit

- Ohio Small Estate Affidavit

- Oklahoma Small Estate Affidavit

- Oregon Small Estate Affidavit

- Small Estate Affidavit Pennsylvania

- South Carolina Small Estate Affidavit

- Tennessee Small Estate Affidavit

- Small Estate Affidavit Utah

- Small Estate Affidavit Virginia

- Washington State Small Estate Affidavit

- Wisconsin Small Estate Affidavit

Lease Agreement Templates

There are countless potential issues with an unprofessional rental agreement, ranging from the inability to evict tenants to huge repair costs or other property damages that otherwise would’ve been avoided. A proper lease agreement and real estate contract are created to ensure that every party understands their rights and responsibilities. Below is the complete list of rental agreement forms and templates that we have put together for your convenience.

The Most Widely Used Lease Agreement Templates

A lease agreement is the basis of successful relationships between landlords and tenants. The agreement usually outlines in detail all tenancy terms and policies. A landlord and tenant should check and recheck their lease agreement and ensure they clearly understand each other. Depending on the renting premises, there are various lease agreement types. The most popular ones are a one-page rental agreement, sublease agreement, rent-to-own agreement, room rental agreement, commercial lease, and roommate agreement. We will look closely at them in the following sections.

Before signing a lease agreement, a landlord wants to learn more about their potential tenants with the help of the Rent Lease Application Form. Along with this form, they can request a tenant to consent to the credit history or background check. It allows landlords to choose their tenants more carefully. Tenants may also take advantage of a rental application form and put their best side forward.

When a landlord finds their perfect tenant, they can sign a Simple Rental Agreement. A simple one-page rental agreement is used only for residential property and includes basic information related to the tenancy such as length of the lease, rent amount, security deposit, and notice requirements. Still, it’s an efficient way to manage landlord-tenant relationships since the agreement provides all the details for a tenant to fulfill their contractual obligations.

If you would like to rent out your property in California, you will have to provide a list of disclosures to your tenant along with signing a California Rental Agreement. They include the lead-based paint disclosure, bedbug addendum, flood disclosure, pest control, mold disclosure, and smoking policy disclosure.

A tenant can rent out the landlord’s premises using a Sublease Agreement Template. It’s concluded between a tenant, also referred to as a sublessor, and subtenant and must be approved by a landlord. This agreement is considered to be the lease within the lease, and the tenant must still comply with the original rental agreement. A sublease agreement comes in handy when the tenant cannot continue to live on the premises and finds another person to rent the property until the original lease expires.

If you want to buy residential property but cannot afford it yet, a good way out is a Lease to Own Agreement. This document is technically a lease agreement but with the option to buy the property at the end of the lease term. That’s why it must include earnest money deposit, purchase price, and how much rent go towards the purchase, apart from standard lease agreement terms and policies.

A Room Rental Agreement Template allows a homeowner or original tenant to rent out or sublet a room. It’s an option for a landlord who wants to lease the rooms in the apartment separately. This document contains all the same terms and provisions that a standard lease agreement would.

Unlike a room rental agreement, a Roommate Agreement Template is concluded between tenants living on the same rental premises. In this case, a landlord is not involved, and tenants use this agreement to manage their financial obligations and household rules. A roommate agreement is considered legally binding, so the tenants should take this document seriously.

In order to rent out a business property, it’s necessary to use a Commercial Lease Agreement Template. Commercial property means property that is not used for residential purposes, for example, offices, restaurants, or warehouses. Usually, the rent for commercial property is calculated as a cost per square foot. A commercial lease agreement lasts longer than a residential one.

A landlord or tenant may decide to end the tenancy earlier than it expires. They are expected to use a Termination of Lease Letter to notify each other of such a decision. A landlord is not obliged to renew the lease but has to provide the tenant with a notice to vacate. The same implies to the tenant – they have to send an intent to vacate. As a rule, a lease agreement should provide notice requirements the landlord or tenant must comply with when deciding to terminate the tenancy early. Here’s a sample to give you a better idea:

State Lease Agreement Templates by Type

A lease agreement is concluded between a landlord and tenant if the latter’s rental application is approved. If you are looking for a specific type of lease agreement or related application forms, check the list below. The documents are divided by both type and state for your convenience.

- California Rental Application

- California Commercial Lease

- California Month to Month Rental Agreement

- California Rent Increase Form

- Room Lease Agreement California

- California Sublease Agreement Template

- Florida Rental Application

- Florida Commercial Lease Form

- Florida Month to Month Lease

- Massachusetts Rental Application

- Greater Boston Real Estate Board Lease

- Rental Application NY

- Sublease Agreement New York

- NC Rental Application

- Texas Rental Application Form

- Texas Commercial Lease Form

- Wisconsin Rental Application

Lease Agreement Templates by State

Lease agreements outline the responsibilities and obligations of a landlord and tenant. State laws require a lease agreement to be in writing and signed by both parties. Some lease terms may vary from state to state, for example, a security deposit amount. Many states have statutory limits on how much money landlords can request as a deposit. These limits usually depend on the rent amount. The following lease agreement templates are prepared considering all essential state requirements.

- Rental Agreement Alabama

- Arizona Rental Agreement

- Rental Agreement Colorado

- Rental Lease Agreement CT

- Florida Lease Agreement

- Rental Agreement Georgia

- Hawaii Lease Agreement

- Lease Agreement Illinois

- Chicago Apartment Lease Form

- Indiana Rental Agreement

- Louisiana Rental Agreement

- Maryland Rental Agreement

- Massachusetts Lease Agreement

- Rental Agreement Michigan

- Rental Agreement MN

- Missouri Residential Lease Agreement

- Nevada Rental Agreement

- Lease Agreement NJ

- New Mexico Rental Agreement

- New York Residential Lease Agreement

- Lease Agreement NC

- Ohio Residential Lease Agreement

- Oklahoma Rental Agreement

- Oregon Lease Agreement

- Rental Agreement PA

- SC Lease Agreement

- Tennessee Rental Agreement

- Lease Agreement Texas

- Utah Lease Agreement

- Rental Lease Agreement Virginia

- Rent Agreement WA

- Wisconsin Residential Lease Agreement

Lease Agreement Types

Renting property requires an accurate lease agreement. Depending on the property type, you will have to prepare a specific agreement. For example, if you would like to rent out your property regularly, you should create a week-to-week or month-to-month rental agreement. If you need space where you could leave your car, consider creating a parking rental agreement. The following lease templates will be helpful for both landlords and tenants.

- Garage Lease Agreement

- Photo Booth Contract

- Salon Booth Rental Agreement

- Commercial Sublease Form

- Venue Contract Template

- Wedding Venue Contract Template

- Condominium Lease Agreements

- Family Rental Agreement

- Hunting Lease Contract

- Month to Month Lease Agreement

- Parking Space Rental Agreement

- Roommate Agreement Dorm

- Short Term Lease Agreement

- Week to Week Rental Agreement

Termination Letter Templates

If you are wondering how to terminate your tenancy earlier than expected, the list below is for you. State laws allow early lease termination if a landlord or tenant notify each other in advance. The notice periods vary from state to state and range from 20 to 60 days. But notice periods and requirements can also be provided directly in the lease agreement.

- Early Termination of Lease Letter

- Arizona 30 Day Eviction Notice

- California 30 Day Notice to Vacate

- 60 Day Notice to Vacate California

- Florida Lease Termination

- 30 Day Notice to Vacate Illinois

- 30 Day Notice of Termination NYC

- Ohio Notice to Vacate

- 30 Day Notice to Vacate Oregon Template

- 30 Day Notice to Vacate Texas Template

- Notice to Vacate Washington State

Other Templates Related to Lease Agreements

The following forms can come in handy if a landlord needs to renew the lease or notify a tenant about a rent increase. In some cases, a landlord has to give a written consent to approve a sublease agreement their tenants will sign. All these situations require specific forms and letters to be filled out, which you will find below.

Eviction Notices

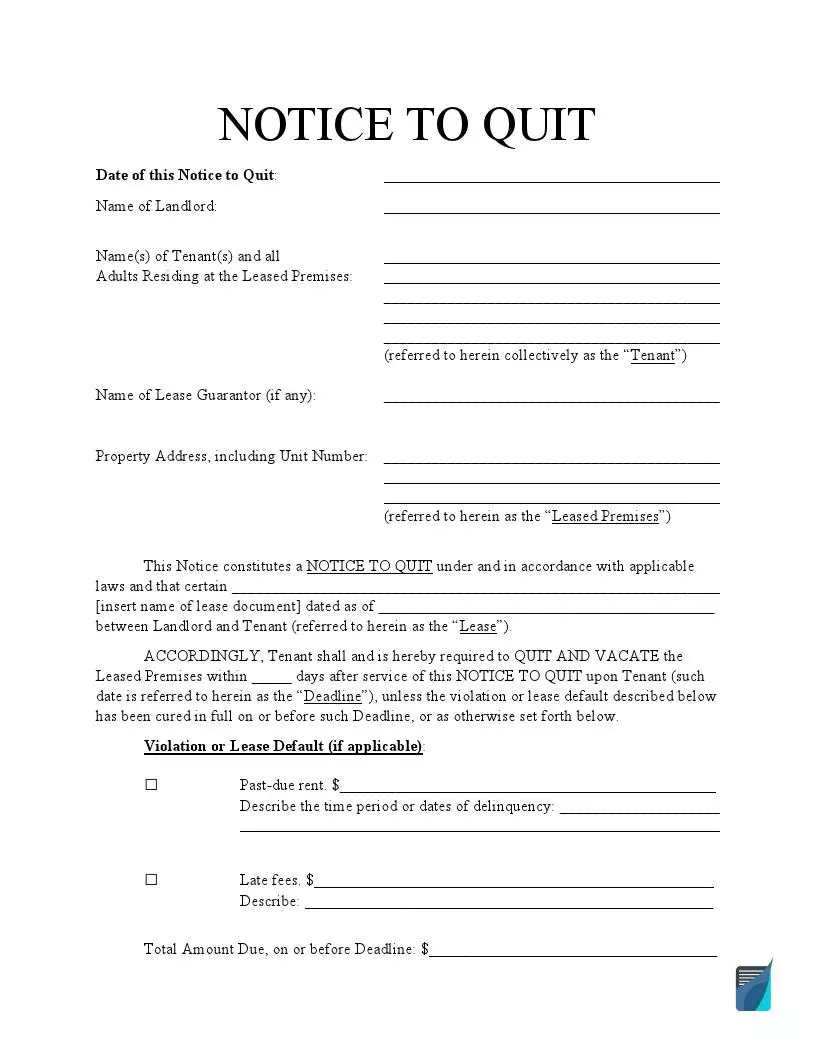

A violation of the lease agreement terms can lead to eviction. Eviction means that a tenant will be removed from the renting premises if they do not fix the problem. However, eviction is not a quick process, and it can take some time before a landlord obtains a writ of possession. To start the process, the landlord should send an eviction notice, also known as a notice to quit, and give the tenant the possibility to cure the situation.

The Most Widely Used Eviction Notices

When sending an eviction notice, a landlord must consider the violation nature, state laws, and agreement’s terms. The notice usually includes the description of the violation, the way to cure it, and the number of days to fix the problem. These notices are called “curable.” But there is also an incurable type of eviction notices, which gives the tenant no other option but to move out.

One of the most frequent notices to quit is a Late Rent Notice Template sent following late rent payment. In this case, the landlord informs the tenant about the amount due to pay, late fees (if any), and the deadline for paying it or leaving. The notice period is usually three to five days. If the tenant ignores the note, the landlord may start the eviction process by addressing the court.

As a rule, a 3 Day Notice to Quit is used to notify the tenant about nonpayment of rent. However, depending on the state, it can also inform about non-monetary default. As the name implies, a 3-day notice to quit gives the tenant only three days to cure the situation or leave the property.

A 60 Day Eviction Notice, in its turn, is sent when the landlord wants to end a month-to-month tenancy. It’s possible to do if the tenant possesses the property for longer than one year. A 60-day notice is considered the most amicable one, as it gives the tenant enough time to find another place to live. But this notice can also be required by state laws.

Such requirements exist in California. The landlord has to send a California Eviction Notice 60 days in advance if they want to terminate a month-to-month lease with the tenant who lives on the premises for a year or more. Otherwise, the landlord can send a 30-day California Lease Termination Letter. For nonpayment of rent or noncompliance with the agreement, the landlord should send a 3-day notice to quit.

In Texas, you can use a Notice to Vacate Texas Form to inform the tenant about possible eviction. Late rent or noncompliance with the agreement requires a 3-day notice, while a lease termination notice is sent 30 days in advance. Texas law allows the landlord to give a 2-day grace period for paying the rent after the due date.

Eviction Notice Types

Eviction notices are divided into types regarding the given time period. These periods usually depend on the violation nature and local requirements. Additionally, these terms can be explicitly provided in the agreement between a landlord and tenant. Note that these terms cannot conflict with the law. For example, if a notice period required by the state is 60 days, the landlord should not provide only 20 days.

- 10 Day Notice to Vacate

- 14 Day Eviction Notice

- 5 Day Notice to Vacate Form

- 7 Day Notice to Quit

- Notice of Noncompliance

Sample Notice to Quit:

Eviction Notices by State

Some states provide landlords with more powers related to eviction. For example, in New Jersey, you can end the tenancy without notice in the case of late rent payments. In some cases, you can send unconditional quit notices that do not allow the tenant to fix the situation. They are applied for severe or repeated violations, such as illegal activities on the premises (distributing drugs, engaging in prostitution or related activities, or using and possessing a firearm without legal permission).

- Alabama Eviction Notice

- Notice to Vacate AZ

- Arkansas Eviction Notice Form

- Colorado Notice to Vacate

- Eviction Notice CT

- Eviction Notice Template Florida

- GA Eviction Notice Form

- Illinois Eviction Notice Form

- Indiana Notice to Quit

- Kansas Notice to Vacate

- Louisiana Eviction Notice

- Maryland Notice to Vacate

- Massachusetts Notice to Quit

- Michigan Notice to Quit

- Minnesota Eviction Notice Form

- Notice to Vacate Missouri

- NJ Notice To Quit

- Eviction Notice Template NY

- NC Eviction Notice Template

- Ohio Eviction Notice Form

- Oklahoma Eviction Notice

- Oregon Eviction Notice Form

- PA Notice to Quit

- SC Eviction Notice Template

- Eviction Notice Tennessee

- Utah Eviction Notice

- Eviction Notice in VA

- Notice to Vacate Washington State

- WV Eviction Notice

- Wisconsin Eviction Notice

State Eviction Notices by Type

If you need a specific state eviction notice form, the following list is for you. These forms are prepared considering state requirements. For example, the landlord needs to send a 3-day notice in California or Florida if the tenant misses a rent payment. Still, in Michigan, you must notify the tenant seven days in advance.

- 3 Day Notice California

- 3 Day Eviction Notice Florida Template

- 30 Day Eviction Notice Florida

- 5 Day Notice Illinois

- Michigan 7 Day Notice

- NYS 3 Day Eviction Notice

- 3 Day Eviction Notice Ohio

- 72 Hour Notice Oregon

- 3 Day Eviction Notice Texas

- 5 Day Notice Wisconsin

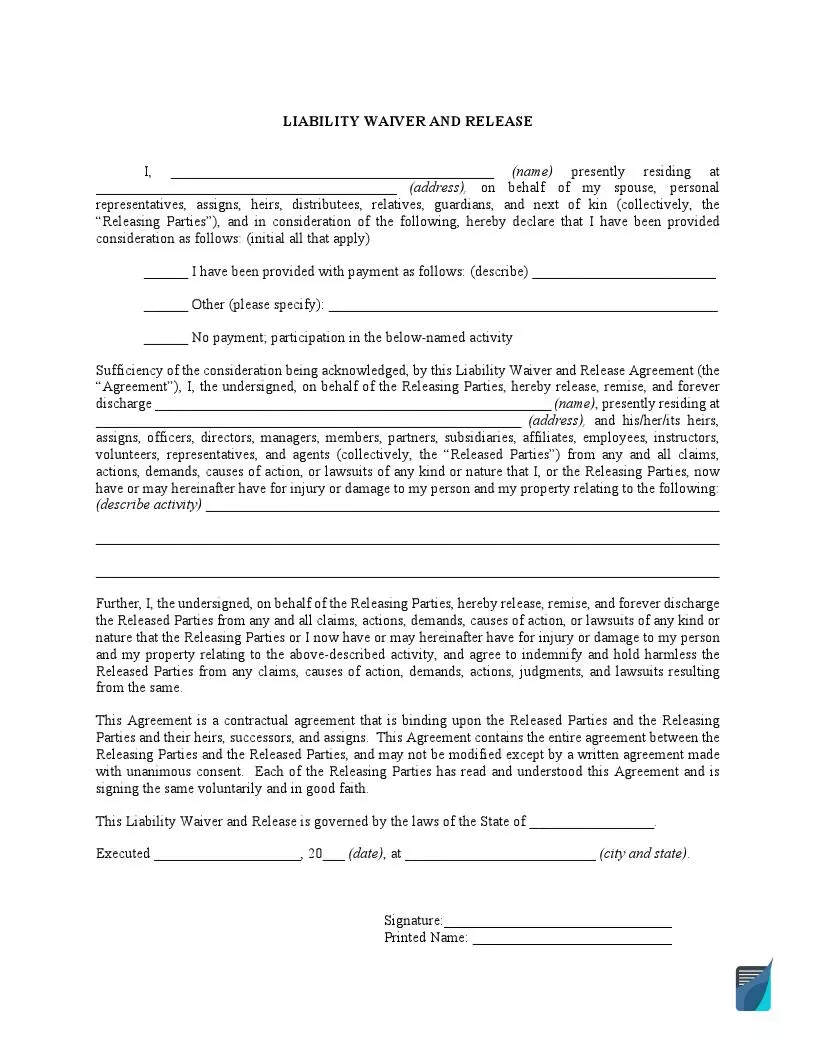

Release Of Liability Templates

A release of liability is a legal document that protects an individual or entity from legal responsibilities. With this document, one party, the releasor, promises not to sue another party, the release. This promise may be related to the physical risk and extreme activities, as well as a car accident. A release of liability can also be used to document a person’s consent to be recorded.

The Most Widely Used Release of Liability Forms

A release of liability can protect the business from possible lawsuits. The document should always include the releasor’s and releasee’s contact information, the event or activity, consideration (if any), effective date, and governing law. The following documents are the most widely used release of liability forms related to future and past events.

One of the most popular releases is a Medical Release Form. The federal Health Insurance Portability and Accountability Act of 1996 (HIPAA) forbids health providers from disclosing a patient’s information without valid authorization. A medical release form gives such authorization and includes the list of individuals, such as family members, friends, or other parties who will have access to a person’s medical records.

A Photo Release Form Template will help you confirm a person’s consent to be photographed or use their photos for personal or commercial purposes. The form ensures that the person is aware of being photographed and agrees to the usage of their images.

A similar to the previous one is a Standard Model Release Form. It aims at getting a model’s consent to pose in pictures. The document is concluded between an artist and a model and is widely used in stock photography, commercials, or clothing modeling.

Another release form related to the entertainment sphere is a Film Release Form Template. It allows an individual or entity to use someone’s likeness recorded in video and photographed. This form can be used for personal or commercial usage. Signing the film release, a person allows a third party to use their likeness and voice.

As mentioned before, a release of liability can be used for past events, for example, a Car Accident Release of Liability Form. The document helps avoid legal responsibility in the event of a car accident. The injured party may agree to sign the release in exchange for compensation and release the liable party from being sued.

Release of Liability Types

If you need to prepare a specific release of liability form, check the list below and choose the one that suits your needs. When creating the document, do not forget to include a description of the event or activity, risks and danger provisions, compensation provisions (if any), effective date, and governing laws.

- Art Release Form

- Release of Liability Form Car

- Interview Release Form Template

- Film Location Release Form

- Conditional Lien Release Form

- Partial Release of Lien

- Unconditional Lien Release

- Media Release Form Template

- Dental HIPAA Release Form

- Mortgage Lien Release Form

- Music Release Form for Film

- Personal Training Waiver and Release Form

- Photography Copyright Release

- Permission to Photograph Form for Daycare

- Employee Photo Consent Form

- Photo Release Form for Minors

- Pet Photo Release Form

- Form SSA 3288

- Talent Release Form Template

- Actor Release Form Template

- Tattoo Waiver Form

- Doctor Release Form

Sample Release of Liability:

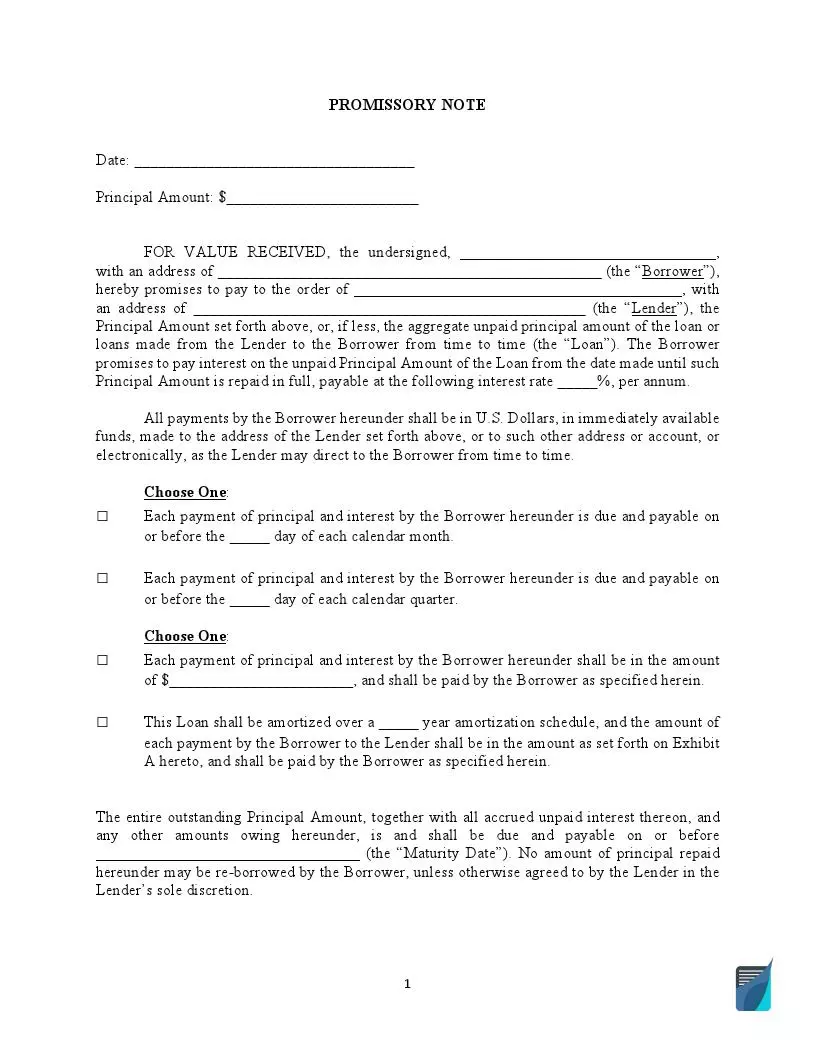

Fillable Promissory Notes

A promissory note is a legal and financial instrument that enforces an individual or entity to repay the borrowed money. A promissory note is often referred to as a loan agreement or IOU but there are slight differences between them. The note can be used in many circumstances, including mortgage, student loans, and business loans. If you want to get a high-quality promissory note, check the forms below and choose the appropriate type.

Popular Promissory Note Forms

A lender is always recommended to use a Secured Promissory Note Template. This note provides collateral security in the form of a car or house. Thus, if the borrower does not repay the money, the lender will get these assets. A secured promissory note offers stronger security for the lender and, as a rule, allows the borrower to pay a lesser interest rate.

If the lender relies on the borrower’s credibility, they can use an Unsecured Promissory Note Template to prepare the document. An unsecured promissory note provides no guarantee for the lender to get the borrowed money back and offers no remedy against failure to pay. If the borrower fails to pay back, the lender will have to file a lawsuit to recover the loan.

If you live in California, you can take advantage of a Promissory Note Template California to create your secure or non-secure promissory note. Like in all states, California promissory notes are governed by the state’s usury laws. In California, it’s possible to charge the maximum interest rate of 10% for family, personal, or household purposes.

Promissory Note Forms by State

A promissory note outlines all the terms and conditions of the loan. The document includes the lender’s and borrower’s contact details, the amount of money being borrowed, the collateral type, repayment schedule, and the interest rate. The annual interest rate may vary from state to state. Each state has its usury laws limiting the interest rate a lender can charge. For example, in California, it’s 10%, but you can only charge up to 7% in Michigan. As the lender, you will need to check the local requirements and select one of the state forms to create an accurate promissory note.

- AL Promissory Note Form

- Promissory Note Arizona

- Colorado Promissory Note

- Connecticut Promissory Note

- Promissory Note Template Florida

- Georgia Promissory Note

- Illinois Promissory Note

- Promissory Note Indiana

- Promissory Note IA

- KS Promissory Note

- Kentucky Promissory Note Template

- Louisiana Promissory Note

- Promissory Note MD

- Massachusetts Promissory Note

- Promissory Note Michigan

- Promissory Note MN

- Missouri Promissory Note

- Promissory Note NV

- NJ Promissory Note

- Promissory Note Template New York

- Promissory Note NC

- Ohio Promissory Note

- Promissory Note Oregon

- Promissory Note SC

- Promissory Note Template Texas

- Utah Promissory Note

- Virginia Promissory Note

- Promissory Note Template Washington State

- Wisconsin Promissory Note

Promissory Note Types

Apart from secured and unsecured promissory notes, there are also a vehicle promissory note and promissory note release. A vehicle promissory note is a binding document that ensures a buyer of the vehicle will pay the purchase price in accordance with the note terms. A promissory note release, in its turn, releases the borrower from all responsibilities and obligations related to the note. This document is usually given when the promissory note terms are entirely fulfilled.

Sample Promissory Note:

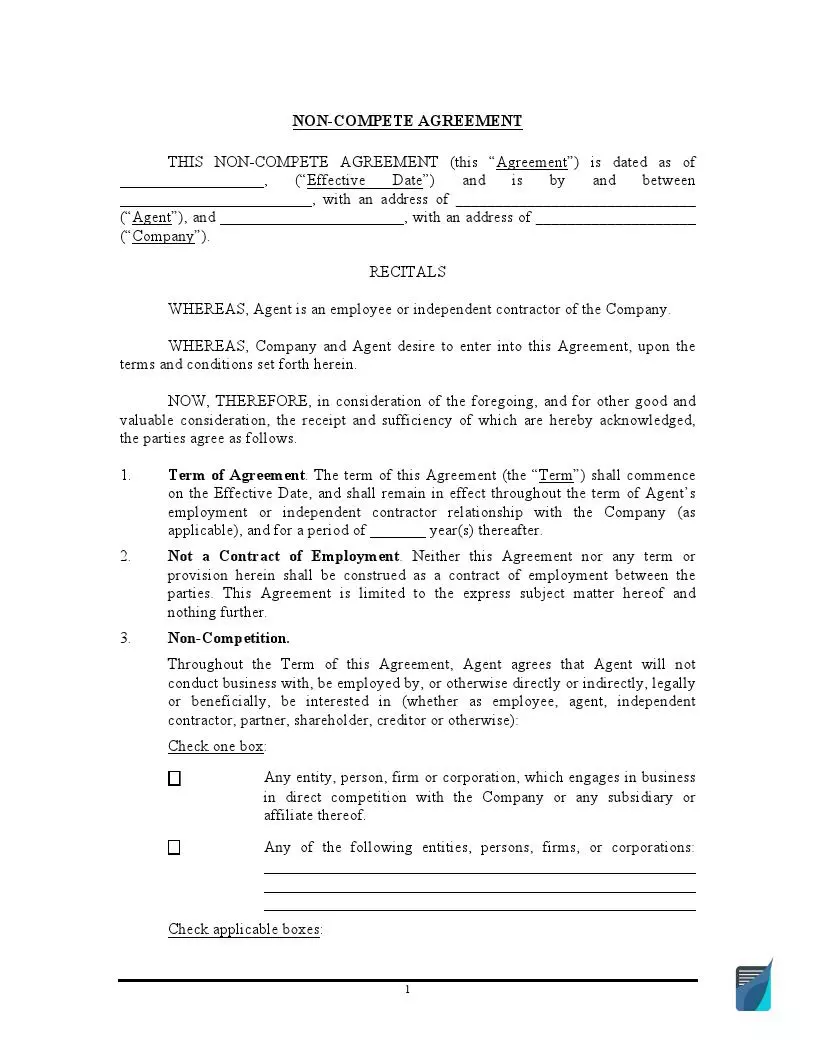

Find Fillable Non-Compete Agreement

A non-compete agreement prevents one party from competing with another party in a specific industry and geographical area. This document is the most common practice when hiring new employees. A non-compete agreement (get our updated NCA here) can serve as additional protection for your business but should have reasonable terms. “Reasonable” means that the agreement duration should not exceed a certain period of time (usually, two years maximum) and should cover only the relevant geographical area.

Popular State Non-Compete Agreement Forms

When it comes to non-compete clauses or non-compete agreements, state laws are not the same. In many states, these agreements are considered void, while in others, you have to comply with strict requirements when creating such an agreement.

A Non Compete Agreement California Template can help you restrict your employees from working for competitors for a certain period or creating a similar business in the same area. But in California, non-compete agreements are generally considered unenforceable. If you want to create a California non-compete agreement, it’s necessary to obtain legal advice.

In Florida, non-compete agreements are allowed to be used by employers as long as they provide reasonable terms. A Non Compete Agreement Florida Template will help you create a valid legal document to protect your company’s sensitive information and intellectual property rights. To be considered reasonable, your Florida non-compete agreement should not last for more than six months.

A Texas Non Compete Agreement is a legally binding document protecting your legitimate business interests. In Texas, non-compete agreements usually provide certain compensation for the employee who agrees to sign the agreement. It comes in the form of a pay raise or promotion. A Texas non-compete agreement is considered reasonable if the agreement’s duration does not exceed two years.

Non-Compete Agreements by State

As mentioned above, a non-compete agreement is a matter of state jurisdiction, so you have to be careful when preparing one. Such agreements cannot be legally binding in North Dakota and Oklahoma. California does not recognize them as well. Many states require non-compete agreements to be reasonable in terms of time limits and geographic scope. The following list of state non-compete forms will help you save time searching all the local requirements.

- Alabama Non Compete Agreement

- Alaska Non Compete Agreement

- Non Compete Arizona

- Arkansas Non Compete Agreement

- Non Compete Agreement Colorado

- Connecticut Non Compete

- Delaware Non Compete Agreement

- Georgia Non Compete

- Non Compete Agreement HI

- Idaho Non Compete

- Non-Compete Agreement Illinois

- Non Compete Indiana

- Iowa Non Compete Agreement

- Kansas Non Compete Agreement

- Kentucky Non Compete

- Louisiana Non Compete

- Non Compete Agreement ME

- Non Compete Maryland

- Non Compete Agreement Massachusetts Template

- Non Compete Michigan

- Non Compete Agreement Minnesota

- Non-Compete Mississippi

- Non Compete Agreement Missouri Template

- Non Compete Agreement Montana

- Non Compete Agreement NE

- Non Compete Nevada

- New Hampshire Non Compete Agreement

- Non Compete Agreement New Jersey

- New Mexico Non Compete Agreement

- Non-Compete Agreement New York Template

- North Dakota Non Compete Agreement

- Ohio Non Compete

- Oklahoma Non Compete Agreement

- Non Compete Oregon

- Non Compete Agreement Pennsylvania

- Non Compete RI

- South Carolina Non Compete

- SD Non Compete Agreements

- Non Compete Tennessee

- Non Compete Agreement Utah

- Vermont Non-Compete Agreement

- Virginia Non Compete Agreement

- Non Compete Agreement Washington

- Non Compete Agreement WV

- Non Compete Wisconsin

- WY Non Compete Agreement

Non-Compete Agreement Types

The primary purpose of a non-compete agreement is to ensure that your employees will not engage in competition that may harm your company and influence its share in the market. It relates to both permanent employees and independent contractors who may access highly sensitive and valuable information during their work. That’s why the following templates can be helpful to protect your company’s interests.

Sample Non-Compete Agreement:

Fillable Prenuptial Agreement

Prenuptial agreements, also known as antenuptial agreements or prenups, outline what will happen to financial assets and debts if the couple decides to divorce. It can come in handy in distinguishing what separate and community property is after the marriage, as well as defining child support and alimony. A prenuptial agreement shows the partners’ serious intention to be together, so it’s worth considering one before getting married.

Popular Prenuptial Agreement Forms

A prenuptial agreement aims at protecting both parties in the event of divorce. That’s why it’s crucial to thoroughly check all the provisions before signing the agreement to avoid being mistreated. Although prenups are legally enforceable documents, the court may still set aside or change some provisions. It’s particularly true to child custody and the amount of child support.

Florida is not a community property state, which means that the marital property and assets will be divided equitably between spouses (not equally). However, a Florida Prenuptial Agreement Form may still be a valuable legal instrument if you want a more active role in deciding marital property distribution in case of divorce or one spouse’s death. The agreement will secure your individual property or family assets, as well as the inheritance of children from a previous marriage(s).

Texas law also allows a couple to enter into a prenuptial agreement. The document includes the spouses’ rights and obligations regarding any property acquired during the marriage and its usage. If you live in Texas and want to be more in control of the marriage’s financial part, you are free to use a Texas Prenuptial Agreement and include there all the relevant provisions.

A California Prenuptial Agreement Form is designed for California residents who want to clarify what will happen to their property and finances after marriage dissolution. California is a community property state, which means that all marital property should be divided equally in the event of divorce. But a prenup will give a couple the possibility to decide on their own what should be divided 50/50 and what should remain separate property.

Prenuptial Agreement Forms by State

All 50 states allow romantic partners to conclude a prenuptial agreement. The majority of states use the Uniform Premarital Agreement Act (UPAA/UPMAA) to determine when and how prenups should be enforced. As a general rule, the agreement should be in writing and signed by both spouses. However, signing requirements may vary from state to state. For example, in New York or New Mexico, you have to notarize the prenup, while you need two witnesses to sign the agreement in Minnesota.

- Prenuptial Agreement AL

- Prenuptial Agreement AK

- Arizona Prenuptial Agreement

- Prenup Agreement in Arkansas

- Prenuptial Agreement Colorado

- Prenuptial Agreements in CT

- Prenup Agreement in Delaware

- Georgia Prenuptial Agreement Form

- Hawaii Prenuptial Agreement Form

- Idaho Prenuptial Agreement Form

- Illinois Prenuptial Agreement

- Prenuptial Agreement IN

- Prenuptial Agreement IA

- Prenuptial Agreement KS

- Prenuptial Agreement in Kentucky

- Prenuptial Agreement Louisiana

- Prenuptial Agreement Maine

- Maryland Prenuptial Agreement

- Prenuptial Agreement Massachusetts Sample

- Prenuptial Agreements in Michigan

- Prenuptial Agreement MN

- Prenuptial Agreement Mississippi

- Missouri Prenuptial Agreement Form

- Prenuptial Agreement in MT

- Nebraska Prenuptial Agreement

- Prenuptial Agreement NV

- Prenuptial Agreement NH

- NJ Prenuptial Agreements

- Prenuptial Agreement NM

- Prenup Agreements New York

- Prenup Agreement NC

- Prenuptial Agreement ND

- Ohio Prenuptial Agreement

- Oklahoma Prenuptial Agreement Form

- Prenuptial Agreement OR

- Pennsylvania Prenuptial Agreement

- Prenuptial Agreement RI

- Prenuptial Agreement SC

- Prenuptial Agreement SD

- Prenuptial Agreement TN

- Utah Prenuptial Agreement Forms

- VT Prenuptial Agreement

- Prenuptial Agreement Virginia

- Washington State Prenuptial Agreement Form

- Prenuptial Agreement WV

- Prenuptial Agreements in Wisconsin

- Prenuptial Agreement Wyoming

Find Fillable Operating Agreement

A limited liability company (LLC) operating agreement defines relations between company members and outlines their rights, obligations, and liabilities. Each operating agreement includes the company name and address, the formation details, its registered agent, ownership type, business purpose, and member capital contributions. Depending on the LLC type, the company may have only one LLC member or several founding members. You can create an operating agreement at any stage of your company’s existence, but it’s always better to do it at the beginning to manage all business decisions properly.

The Most Widely Used Operating Agreement Forms

Operating agreements set out the terms of LLCs under the specific owners’ needs. Companies that do not have operating agreements have to comply only with state laws and rules. However, these rules can be too general to control the LLC effectively. So, it’s worth creating one to protect and manage your business. There are two main types of LLC operating agreements – single-member and multi-member.

A Single Member Operating Agreement is designed for a company with only one founding member (owns 100% capital interest). The document helps establish the company’s status separately from the owner’s assets and protects these assets from the LLC’s debts and obligations. A single-member operating agreement is recommended to sign in the presence of a notary public since there is only one person who will sign the form.

If your LLC has more than one funding member, then you will need a Multi Member LLC Operating Agreement Template to create your document. This form is crucial for providing clear communication between all company members and avoiding potential misunderstandings or disputes. A multi-member LLC operating agreement is also recommended to be signed in the presence of a notary public with the copies distributed among all LLC members.

An operating agreement is not required in Florida, but you can use an LLC Operating Agreement Florida to define how your company will be managed. It will help you outline the LLC governing structure and all members’ responsibilities and expectations. Additionally, a FLorida LLC operating agreement will be useful in the event of legal disputes.

Having an operating agreement in California is required by state law. An Operating Agreement LLC California Template is designed to not only fulfill the state requirements but also to protect your LLC status. Although California law requires the LLC’s owner to have an operating agreement, it does not oblige them to file it. The form defines the LLC terms and rules and should be kept internally.

An LLC Operating Agreement Texas is a legal document to define procedures and rules of the LLC registered in Texas. It protects the personal assets and accounts of the LLC members from being financially liable in the event of legal disputes. A Texas LLC operating agreement is not required by law but serves to create a suitable LLC governing structure.

Operating Agreement Forms by State

As a rule, companies’ owners are not legally obliged to create operating agreements. Still, a few states may require you to have an LLC operating agreement. These states are California, Delaware, New York, Maine, and Missouri. Even if an operating agreement is not required in your state, it’s recommended to have one because it allows you to control your business as you wish. Check the forms below and choose the operating agreement template according to the state you live in.

- Alabama LLC Operating Agreement

- LLC Operating Agreement Alaska

- Arizona LLC Operating Agreement

- Operating Agreement LLC Arkansas